BenevolentAI (“BenevolentAI” or the “Company” or the “Group”) (Euronext Amsterdam: BAI), a leading, clinical-stage AI-enabled drug discovery and development company, announces its unaudited preliminary results for the year ended 31 December 2022.

Joanna Shields, Chief Executive Officer of BenevolentAI, said:

“With the world’s attention on AI applications that deliver real-world impact, our progress in 2022 strongly positions BenevolentAI to capitalise on this moment. Our AI platform is proven to enhance drug discovery, as demonstrated by our growing pipeline and successful collaboration with AstraZeneca. Notable clinical and commercial milestones during the period include completing recruitment for our Phase II trial for BEN-2293, submitting the CTA for BEN-8744 and delivering an additional three novel targets to AstraZeneca’s portfolio.”

Operational highlights (including post period)

- Delivered performance enhancements across the Benevolent Platform™

- Introduced the next generation Knowledge Graph, powered by advanced natural language processing (NLP) to enable more precise predictions

- Expanded Target ID tools to discover targets best prosecuted via alternative modalities

- Substantially improved our suite of target identification tools; introduced sophisticated large language models to predict novel therapeutic drug targets from scientific literature

- Launched a product for target progressibility assessments, enhancing R&D decisions across factors like druggability, selectivity and competitor and patent landscapes

- Achieved sustained progress in our platform-generated clinical and pre-clinical pipeline

-

BEN-2293

-

A topical potentially best-in-class PanTrk inhibitor in development to relieve inflammation and rapidly resolve the itch in patients with atopic dermatitis (AD)

-

Completed a Phase IIa study and expect top-line data by the end of March 2023

-

-

BEN-8744

-

An oral peripherally-restricted small molecule PDE10 inhibitor under development as a first-in-class treatment for ulcerative colitis (UC) and with potential for other indications within inflammatory bowel diseases

-

Submitted a Clinical Trial Application (CTA) to the UK Medicines and Healthcare Products Regulatory Agency (MHRA) in December 2022, and expect to initiate a Phase I clinical trial in H1 2023

-

-

BEN-28010

-

An orally administered asset under development as a best-in-class treatment for glioblastoma multiforme (GBM)

-

Declared as a clinical candidate in July 2022, with preparation for IND-enabling studies ongoing

-

The asset could be ready for Phase I studies in 2024

-

-

- Grew our pre-clinical pipeline

-

Transitioned three assets into lead optimisation

-

Generated four new drug programmes using the Benevolent PlatformTM

-

- Delivered strong performance in commercial Target ID collaboration with AstraZeneca

- Delivered three additional novel targets discovered using the Benevolent Platform™ to AstraZeneca’s drug discovery portfolio

- A total of five novel targets, two for chronic kidney disease (CKD) and three for idiopathic pulmonary fibrosis (IPF), have now been validated and selected for portfolio-entry by AstraZeneca

- Each novel target selected by AstraZeneca has the potential to generate significant milestones and royalties for BenevolentAI

- In January 2022, the collaboration was extended for a further 3 years to include heart failure (HF) and systemic lupus erythematosus (SLE)

- Eli Lilly achieved full FDA approval for baricitinib in May 2022. BenevolentAI scientists first identified baricitinib as a COVID-19 treatment using the Benevolent Platform™ in January 2020

-

Initiated a non-commercial collaboration with the Drugs for Neglected Disease initiative (DNDi) and with Stanford University-based Helix Group

-

Made new appointments to strengthen the experience on BenevolentAI’s Board

- In April 2022, Dr Oliver Brandicourt, former CEO of Sanofi and Jean Raby, Partner at Astorg, appointed to the Board as a part of the Business Combination.

- Global ethics and governance expert, Dr Susan Liautaud joined the Board in June 2022

- Kenneth Mulvany and Michael Brennan, two of the Company’s co-founders, stepped down from their positions as Non-Executive Directors.

- Post period, in January 2023, the Board appointed Jean Raby to an additional new role as Senior Independent Non-Executive Director and Dr John Orloff to an additional new role as Workforce Non-Executive Director.

Financial highlights

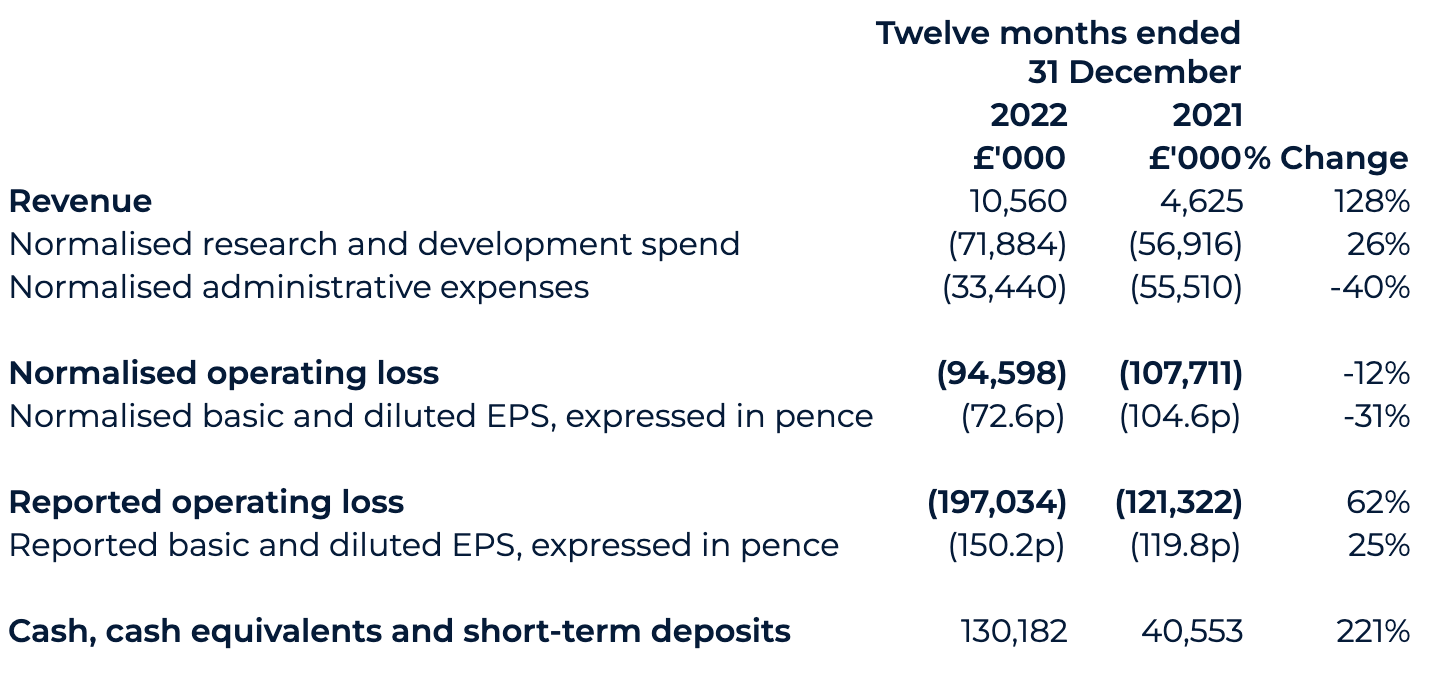

- Revenue increased to £10.6 million (2021: £4.6m), primarily reflecting increased revenues from the AstraZeneca collaboration

- £12.1 million R&D tax credits received in the period

- Completed business combination and listing on Euronext Amsterdam in April 2022 raising £186.8 million (€225 million) gross proceeds.

- Net cash, cash equivalents and short-term deposits position of £130.2 million as of 31 December 2022 at the top end of market guidance (2021: £40.6m)

- Maintained cash runway to Q4 2024, despite inflationary headwind

Analyst and Investor briefing

Management will host an analyst briefing at 9.30 am this morning, 16 March 2023, at the offices of FTI Consulting (200 Aldersgate, Aldersgate Street, London, EC1A 4HD, United Kingdom). To register your interest in attending either in person or virtually, analysts should contact FTI Consulting at BenevolentAI@fticonsulting.com.

A recording of the webcast will be made available in the investor section of the Company’s website shortly afterwards.

About BenevolentAI

BenevolentAI (AMS: BAI) is a leading, clinical-stage AI-enabled drug discovery and development company listed on the Euronext Amsterdam stock exchange. Through the combined capabilities of this AI platform, its scientific expertise, and wet-lab facilities, BenevolentAI is well-positioned to deliver novel drug candidates with a higher probability of clinical success than those developed using traditional methods. The Benevolent Platform™ powers the Company’s in-house drug pipeline and supports successful collaborations with AstraZeneca, as well as leading research and charitable institutions.

Forward-looking Statements

This release may contain forward-looking statements. Forward-looking statements are statements that are not historical facts and may be identified by words such as "plans", "targets", "aims", "believes", "expects", "anticipates", "intends", "estimates", "will", "may", "should" and similar expressions. Forward-looking statements include statements regarding objectives, goals, strategies, outlook and growth prospects; future plans, events or performance and potential for future growth; economic outlook and industry trends; developments in BenevolentAI’s markets; the impact of regulatory initiatives; and/or the strength of BenevolentAI’s competitors. These forward-looking statements reflect, at the time made, BenevolentAI’s beliefs, intentions and current targets/aims. Forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. The forward-looking statements in this release are based upon various assumptions based on, without limitation, management's examination of historical operating trends, data contained in BenevolentAI’s records, and third-party data. Although BenevolentAI believes these assumptions were reasonable when made, these assumptions are inherently subject to significant known and unknown risks, uncertainties, contingencies and other important factors which are difficult or impossible to predict and are beyond BenevolentAI’s control. Forward-looking statements are not guarantees of future performance, and such risks, uncertainties, contingencies and other important factors could cause the actual outcomes and the results of operations, financial condition and liquidity of BenevolentAI or the industry to differ materially from those results expressed or implied by such forward-looking statements. The forward-looking statements speak only as of the date of this release. No representation or warranty is made that any of these forward-looking statements or forecasts will come to pass or that any forecast result will be achieved.

CHIEF EXECUTIVE’S STATEMENT

I joined BenevolentAI as Chief Executive Officer nearly five years ago with a mission to align emerging technologies with science in a bold new way. Today, our ground-breaking AI platform is helping to drive a transformation in drug discovery by empowering scientists to uncover novel targets across many therapeutic areas for different modalities.

Our progress in 2022 has solidified our leadership in the sector as we continued to advance our in-house pipeline and enhance our AI drug discovery platform, the Benevolent Platform™. Commercially, we delivered solid performance in our highly productive collaboration with AstraZeneca, an important revenue driver for the Company, which provides strong scientific and commercial validation of our approach. During the period, AstraZeneca selected three additional novel targets for its portfolio, bringing the total to five novel targets selected to date, and extended the collaboration agreement for a further three years and in two new disease areas. This expansion of our collaboration led to a significant cash investment by AstraZeneca into the business as part of the Business Combination.

Discovery and development portfolio

At BenevolentAI, our AI platform enables scientists to unravel the biological mechanisms underlying complex multifactorial diseases. Using our platform, we have generated a portfolio of 15 named drug programmes and more than ten exploratory programmes, representing a healthy balance of potentially first-in-class and best-in-class assets. This includes BEN-2293, which we are currently progressing through a Phase Ib/IIa clinical study as a treatment for mild and moderate atopic dermatitis, with results expected in the first quarter of 2023. We filed a clinical trial application (CTA) in 2022 for our next most advanced programme, BEN-8744, for ulcerative colitis, with the objective to complete the Phase I clinical study by H1 2024 before initiating a Phase II study. Whilst the Benevolent Platform™ is disease-agnostic, with the unique ability to rapidly identify novel targets in any disease area, going forward, we will focus our internal development pipeline on three core strategic areas: immunology, neurology and oncology, as announced in September 2022. We look to co-develop or out-license the programmes that are outside these therapy areas.

Product and technology

Throughout the year, we delivered performance enhancements to our world-leading AI drug discovery platform. We enhanced our data foundations by launching our next-generation Knowledge Graph, which is powered by advanced natural language processing (NLP) to enable more precise target predictions. We also substantially improved our suite of target identification tools, allowing scientists to discover targets best prosecuted via alternative modalities, and introduced sophisticated large language models (LLM) to predict novel therapeutic drug targets from scientific literature. Finally, we improved R&D decisions by launching a powerful new tool that enables scientists to make target progressibility assessments based on factors like druggability, selectivity and competitor and patent landscapes.

These improvements to our transformative, scalable technology infrastructure have played a pivotal role in delivering key milestones in 2022 through our in-house pipeline and our successful collaboration with AstraZeneca.

Nurturing continuous innovation

Innovation is at the centre of everything we do, and 2022 reinforced our commitment to creating the conditions for innovation to flourish at BenevolentAI. Building on the legacy of our monthly ‘Challenge Days’ – set up during the pandemic – we brought our entire team together for Innovation Week 2022 hosted at our London headquarters for an intensive five days of cross-functional collaboration, which resulted in significant product enhancements, new development projects and enriched team cohesion.

Our collaborations with academic innovators further multiply our opportunities for impact. In the first half of 2022, we initiated phase two of our AI research partnership with the Stanford University-based Helix Group, which focuses on discovering more effective methods to extract knowledge from biological and clinical information. Our innovation pipeline feeds into our intellectual property portfolio, including 91 tech-related applications and 122 drug discovery patent applications, representing an important strategic asset for BenevolentAI.

Impact

BenevolentAI is a purposeful company, and we believe it is important to amplify the impact of our platform and put our technology to good use for wider societal benefit. While our core strategy is to discover novel targets and develop better treatments through our in-house pipeline and partnerships, our non-commercial deployments compliment this core mission in the interest of the global good. One of the most visible applications of our approach was in support of the global campaign against COVID-19. This year we received further validation of the results of AI-enabled research, Baricitinib, the drug identified by BenevolentAI as a treatment for COVID-19 in January 2020, was fully approved by the US Food and Drug Administration (FDA). Baricitinib has been a mainstay of treatment in hospitals globally since being approved for emergency use by the FDA in November 2020, and its success in saving the lives of critically ill COVID-19 patients is a testament to the power of our platform and its potential to enhance and accelerate life-saving research.

Further underscoring our commitment to using our platform for broader societal benefit, we signed a new not-for-profit partnership with the Drugs for Neglected Diseases initiative (DNDi) in 2022. The partnership aims to identify targets and approved drugs that could be used to treat dengue fever, a climate-sensitive neglected disease representing one of the top ten threats to global public health worldwide.

Outlook

Completing our business combination and successfully listing on Euronext Amsterdam in April 2022 was a testament to the strength of our business and growth story. As a result, we closed 2022 in a strong financial position, with a cash runway to Q4 2024 and sufficient capital to support our pipeline and strategy to drive long-term value creation.

We have several value inflection points both in the near and medium term. We expect top-line results of the Phase IIa clinical study for BEN-2293 in Q1 2023, and subject to results we will focus on out-licensing of BEN-2293 for atopic dermatitis post-Phase IIa data and initiate a Phase I study for BEN-8744 for ulcerative colitis in H1 2023. We also plan on delivering one to two CTA or IND-stage drug candidates. We expect to commence IND-enabling studies for at least one additional asset whilst transitioning three projects into lead optimisation, initiating four new drug discovery programmes. We also aim at signing an additional collaboration in the year ahead.

2023 has the potential to be a breakthrough year for BenevolentAI. With the world’s attention on AI applications that deliver real-world impact, we are strongly positioned to capitalise on this moment. With our substantial portfolio of platform-generated drugs, our work with big pharma and research collaborators, and our continued investment in state-of-the-art technology, we are showing every day how AI can be used to unlock the next wave of biopharma innovation.

We believe our leading platform will empower scientists to uncover novel treatments faster and with a higher probability of clinical success. Ultimately, our ambition is to facilitate the scaled development of new, more effective treatments for the patients who need them. I am confident in our ability to deliver on this mission.

Joanna Shields

Chief Executive Officer

FINANCIAL REVIEW

We have delivered a strong operational performance, achieving the majority of our strategic objectives within budget and ending the year with cash at the top end of our stated guidance. With the business combination completed (notes 2.4 and 4 of the financial statements) and the Company listed on Euronext Amsterdam in April 2022, we are in a strong position to deliver on our stated objectives and to create shareholder value.

In 2023 we look forward to the results of BEN-2293 within atopic dermatitis and the upcoming Phase I study of BEN-8744 in ulcerative colitis while also continuing to drive progress across our broader development pipeline. We will also continue to invest and drive innovation across our Product & Technology stack in a targeted manner to retain our differentiated position. Against a macroeconomic backdrop of rising inflation and increasing financial pressures, we have reviewed and refined our spend profile to keep to our stated cash runway target of Q4 2024 whilst still delivering on the predefined objectives as at our interim results.

Revenues

At BenevolentAI, we aim to monetise our platform through commercial collaborations and through developing our pipeline of wholly-owned assets with the aim of out-licensing, co-developing/co-commercialising or, potentially, eventually, commercialising in-house.

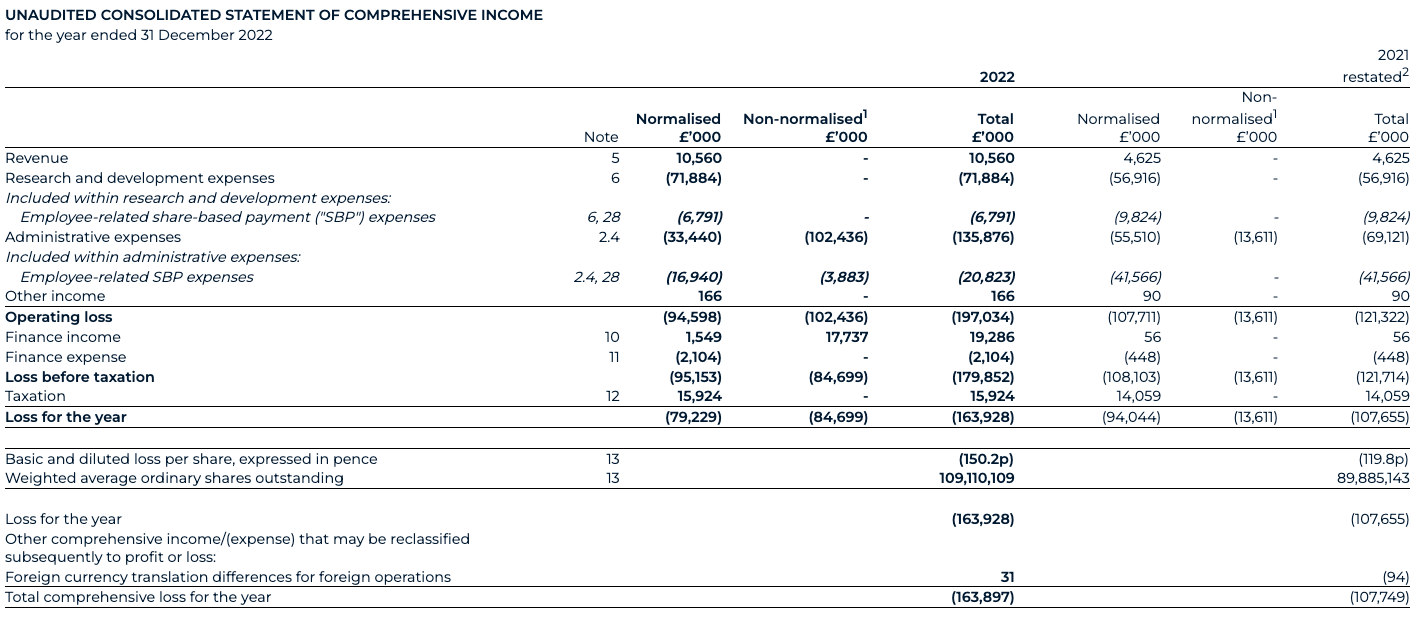

The Group’s revenues increased by £6.0 million to £10.6 million (2021: £4.6 million), primarily reflecting increased revenues from the AstraZeneca collaboration and the majority of this increase reflecting a second AI-enabled drug discovery collaboration that started in January 2022, combined with revenue from a one-year extension to the initial collaboration that began in late 2021. We also recognised three milestone payments in 2022 as AstraZeneca selected three additional novel targets in chronic kidney disease (one target) and idiopathic pulmonary fibrosis (two targets).

Alternative performance measures and normalised presentation

The normalised presentation of the Group performance can be found in the Consolidated statement of comprehensive income and explained further in note 2.4 of the financial statements.

Research and development (R&D) expenses

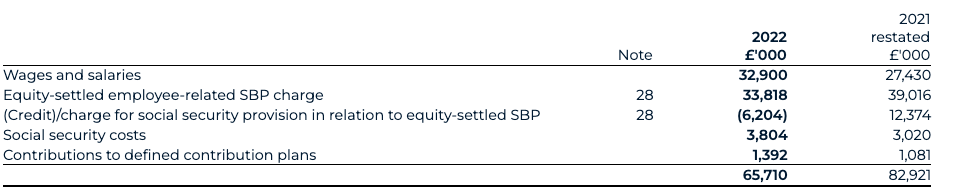

The Group’s investment in R&D is vital to its long-term growth strategy. Our spend can be split across two verticals: 1) Product & Technology, which helps scientists understand complex biology, predict targets and help design and develop drugs for disease and 2) Drug Discovery, where our team of scientists then use our technology stack to pick novel targets for disease before developing drugs for these targets. The output of this symbiotic relationship is in the form of collaborations, such as with AstraZeneca and our pipeline of now 15 named programmes. The normalised presentation of the Group performance can be found in the Consolidated statement of comprehensive income and explained further in note 2.4 of the financial statements.

Normalised product and technology spend, excluding share-based payments, for 2022 increased to £21.9 million (2021: £20.0 million) due to increased staff-related costs to support the continued expansion of the Benevolent Platform™. Reported product and technology spend in 2022 decreased to £24.3 million from £25.1 million in 2021 reflecting lower share-based payment expenses.

Normalised drug discovery spend, excluding share-based payments, for 2022 increased to £43.2 million (2021: £27.1 million). Reported drug discovery spend for 2022 increased to £47.6 million (2021: £31.8 million). The normalised increase was driven by advancing the BenevolentAI pipeline into later stages of development, particularly BEN-2293 and its progression through an adaptive Phase I/II clinical study, alongside BEN-8744 CTA filing enablement in December 2022. We also added a net 4 named programmes into our pipeline during the year.

General and administrative costs

With the business listing in 2022, we have made targeted investments in our operational structures to support our status as a listed business, particularly across finance, compliance, legal and risk activities. The Group continues to make material investments in building and protecting its IP portfolio (consisting of patents, trade secrets, copyright and trademarks). Finally, post-year end, we have also increased investment in our business development capabilities as our pipeline matures and reaches key value inflection points. Normalised business operations spend, excluding employee-related share-based payments, for 2022 has increased to £16.5 million (2021: £13.9 million). Reported business operations spend, excluding employee-related share-based payments, for 2022 has increased to £115.0 million from £27.6 million in 2021. The normalised increase reflects those additional costs related to listing readiness and operating as a public company highlighted above. These costs are expected to stay at these levels given the enhanced level of compliance and reporting obligations and previously discussed investments.

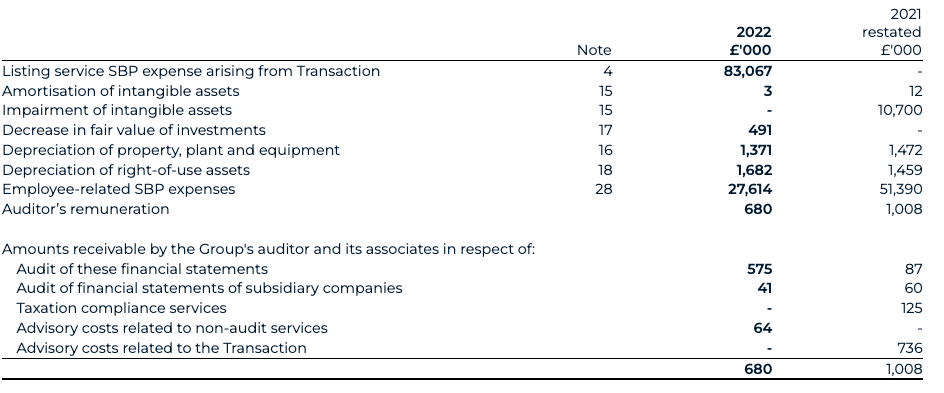

Share-based payments (SBPs)

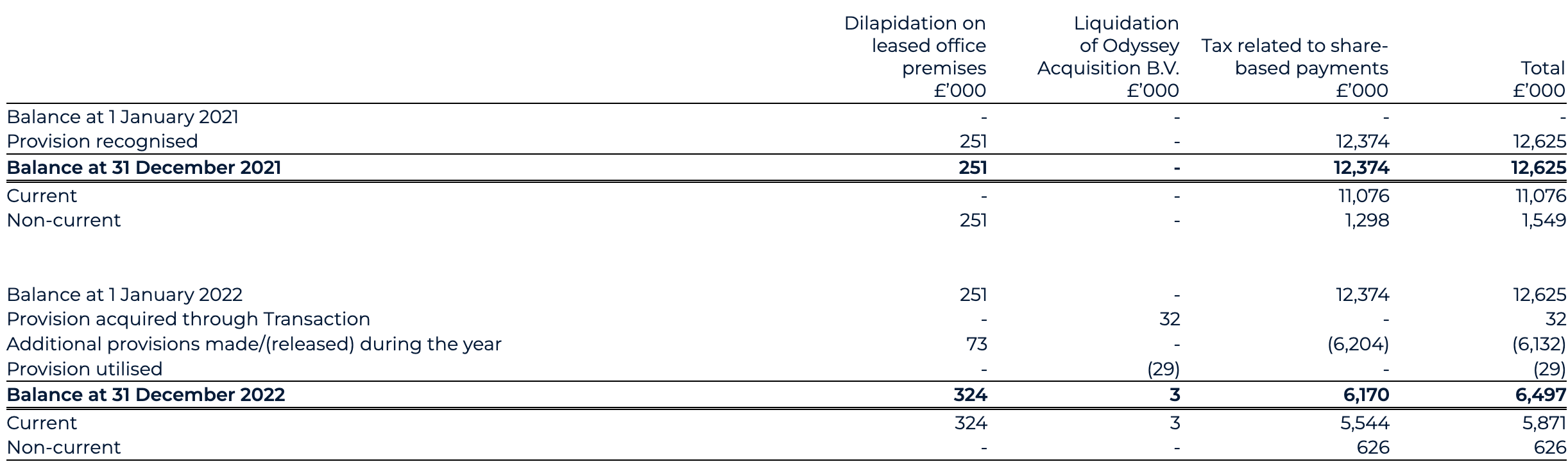

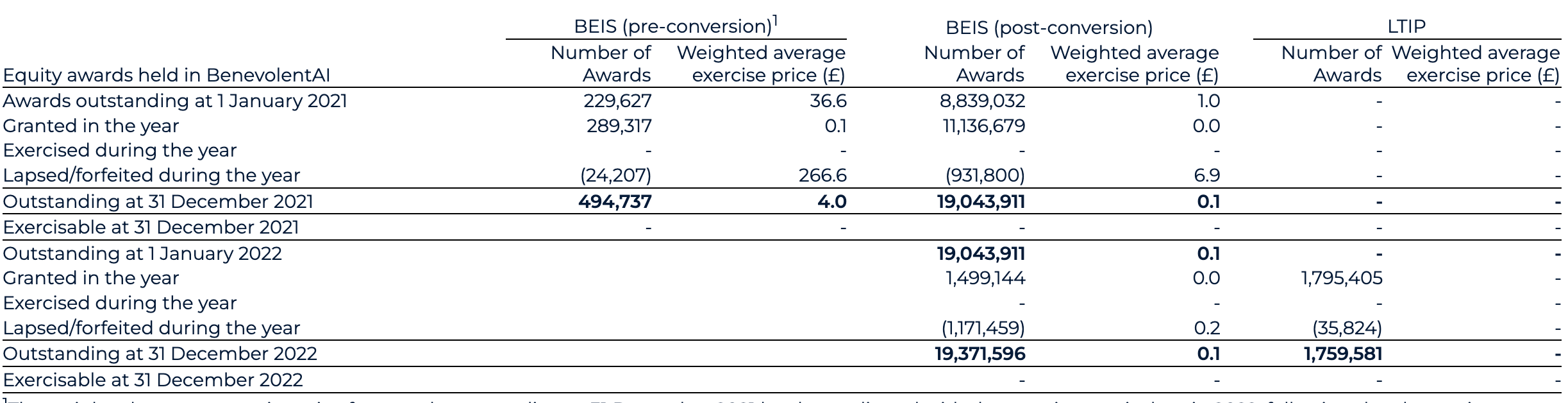

Normalised SBP spend for 2022 has decreased to £23.7 million (2021: £51.4 million). Reported SBP spend for 2022 has decreased to £27.6 million (2021: £51.4 million). The normalised change is predominantly driven by the recognition of vested options under the legacy BEIS share incentive scheme for 2022 of £22.4 million (2021: £51.4 million). This includes a £6.5 million credit in relation to employer-related taxes in 2022 (2021: £12.4 million charge on initial recognition). In 2022, the Group initiated a new LTIP for which a £1.3 million charge has been recognised and which is expected to incur an ongoing SBP charge, inclusive of employer-related taxes, of between £6.2 million and £9.0 million based upon the share price as at the end of December.

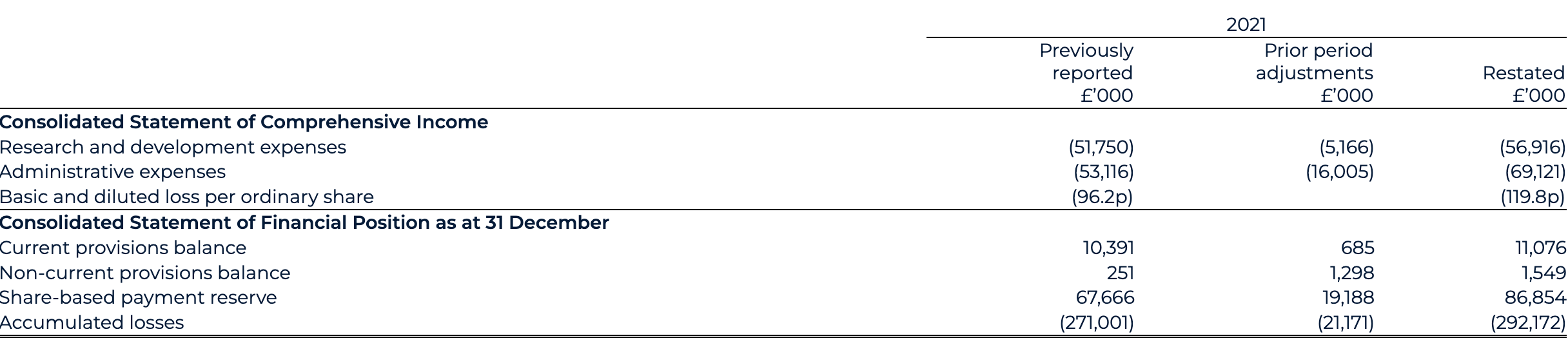

The fair value charging methodology for the legacy BEIS plan has been re-assessed to reflect a now-known “point of exit” and a graded vesting profile. This correction has resulted in an additional £21.2 million SBP charge and restatement to 2021 profit and loss, with a corresponding credit to the share-based payment reserve and employer-related tax provision on 31 December 2021.

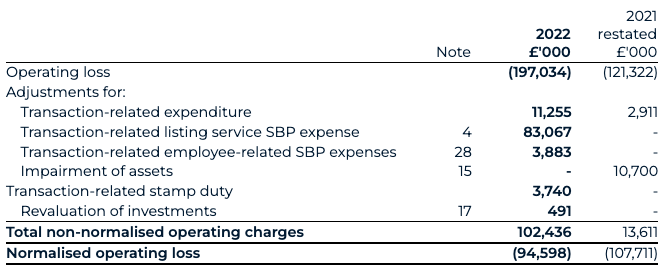

Operating loss

Normalised operating loss for 2022 decreased to £94.6 million (2021: £107.7 million). The reported operating loss for 2022 increased to £197.0 million (2021: £121.3 million) primarily due to the costs arising from the business combination, which are not expected to continue in 2023.

Finance income

Finance income for 2022 has increased to £19.3 million (2021: £56,000). This is predominantly driven by the fair value revaluation of the warrant liabilities acquired through the Transaction, reflecting an increase in their value as of 31 December 2022 compared to the Transaction date of £17.7m.

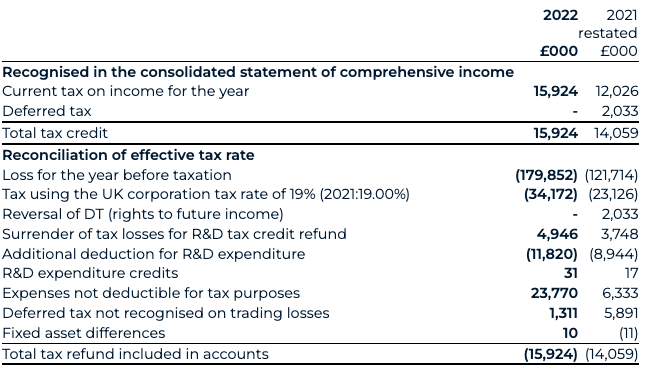

Taxation

Taxation income for 2022 has increased to £15.9 million (2021: £14.1 million). This is predominantly composed of tax credits arising from the UK’s small and medium-sized enterprises' R&D tax relief regime, for which there has been increase in the claim between the two periods, driven by an increase in eligible R&D expenditure.

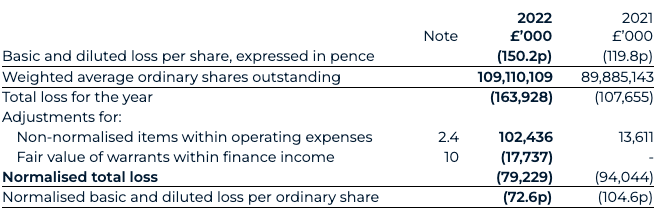

Loss per share

Normalised basic loss per share has decreased to 72.6 pence for 2022 (2021: 104.6 pence), with the weighted average number of shares in both periods adjusted to reflect the exchange ratio of the share for share exchange completed during the Transaction, such as to reflect the capital structure of the legal parent. The increase reflects the decrease in normalised total loss.

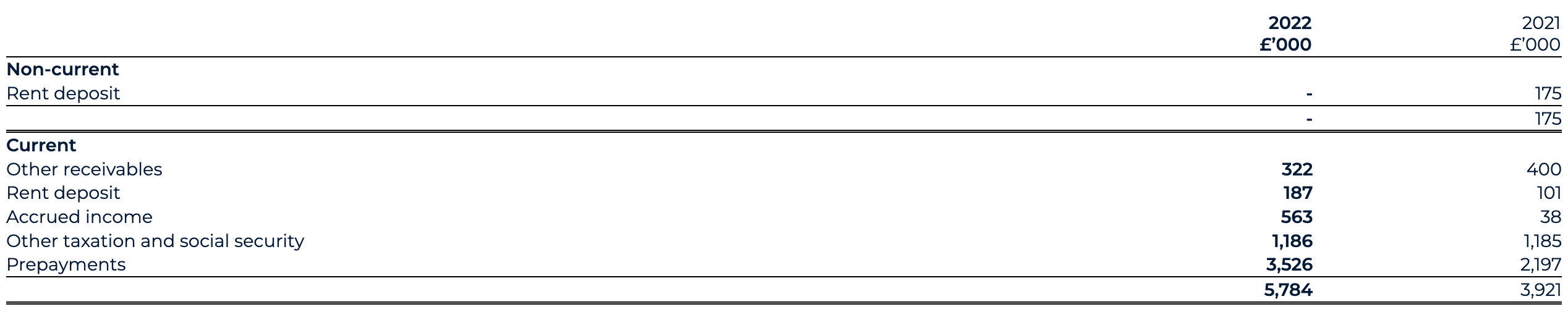

Current assets

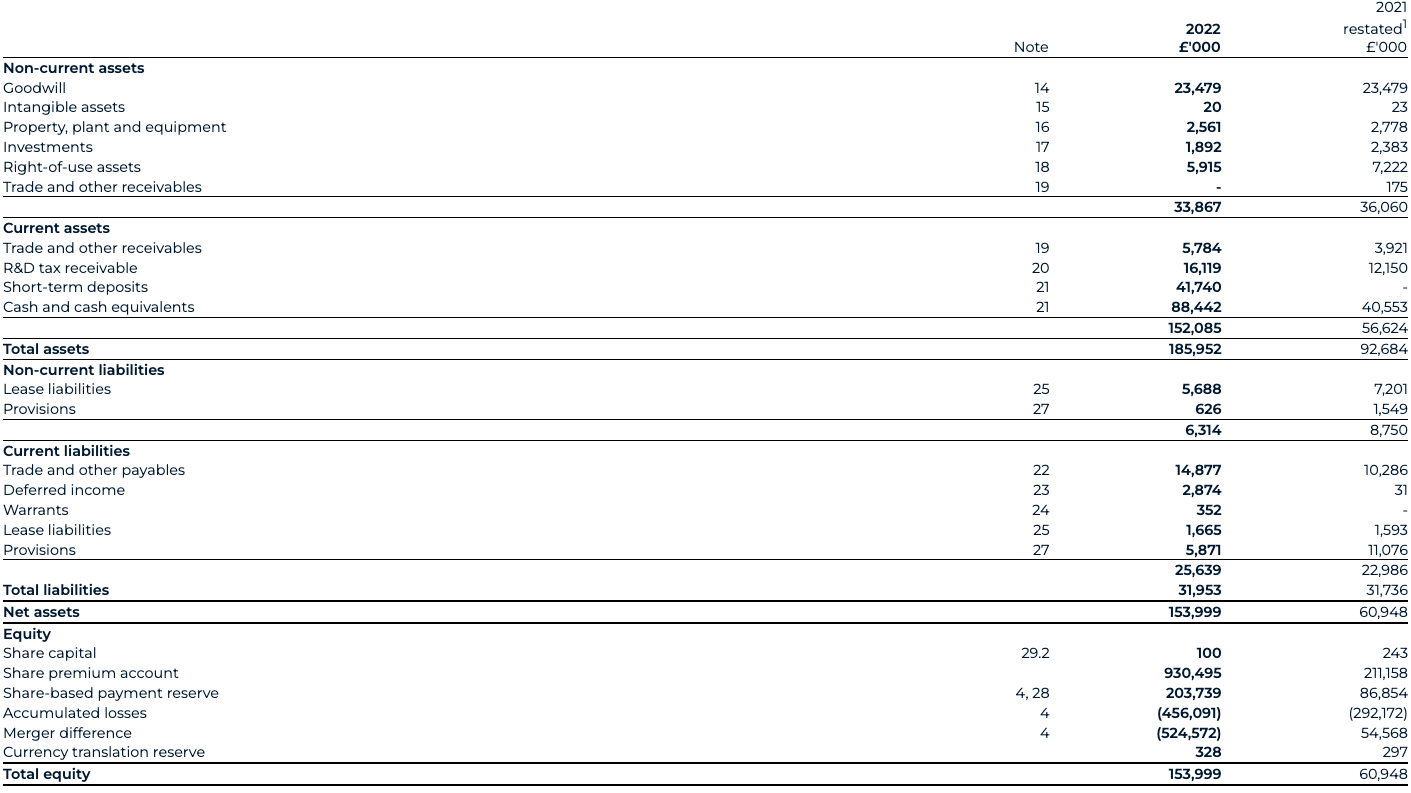

Current assets as of 31 December 2022 have increased to £152.1 million (31 December 2021: £56.6 million), largely driven by an £89.6 million increase in cash, cash equivalents and short-term deposits.

Cash, cash equivalents and short-term deposits

The cash position, including short-term deposits position as of 31 December 2022 has materially strengthened to £130.2 million (31 December 2021: £40.6 million). The PIPE drives this increase, backstop proceeds, Odyssey Acquisition acquired cash, with gross proceeds of £186.8 million (€225 million) and AstraZeneca collaboration proceeds, offset by the settlement of Transaction expenses and ordinary course working capital expenditure.

Warrants

Warrants as of 31 December 2022 have decreased to £0.4 million post transaction close (31 December 2021: £nil), part of the net assets acquired through the Transaction and revalued at the end of the reporting period.

Other current liabilities

Other current liabilities as of 31 December 2022 have increased to £25.3 million (31 December 2021: £23.0 million), reflecting an increase in trade payables for R&D-related expenses as part of the Group’s core activities and an increase in deferred income under the AstraZeneca agreements.

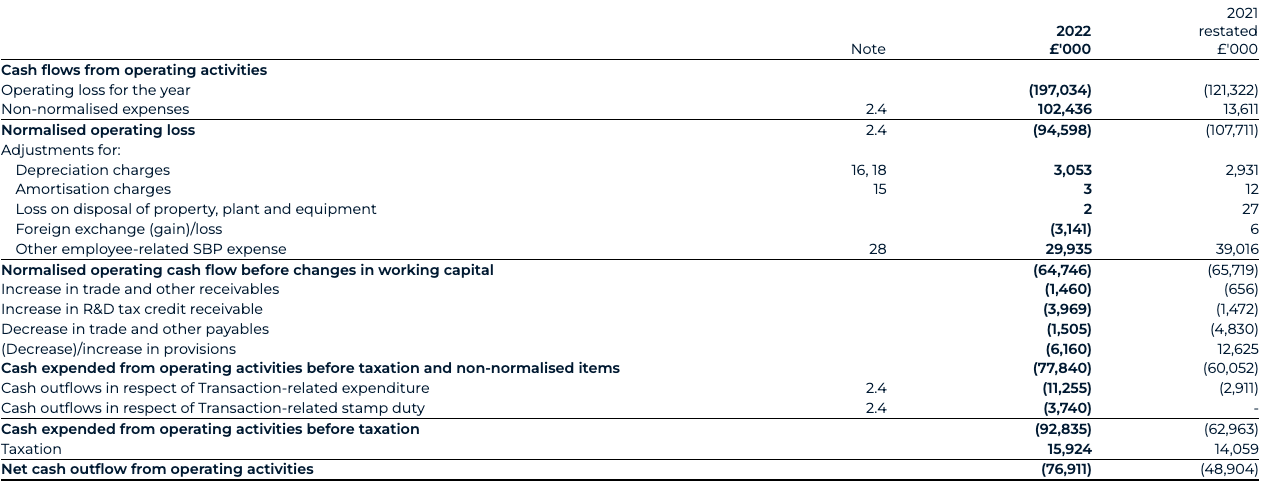

Normalised cash flow

Cash expended from operating activities before taxation and Transaction-related items have increased to £77.8 million for 2022 (2021: £60.1 million), primarily driven by normalised operating losses of £94.6 million.

Dividend

No dividend has been proposed for the year ended 31 December 2022 (2021: nil)

Accounting policies

The Group’s consolidated financial information has been prepared in accordance with international accounting standards, as applicable to the EU, in conformity with the requirements of Luxembourg law. The accounting policies used in the consolidated financial information are consistent with those in the audited financial statements.

Going concern

After making enquiries and/or producing cash flow forecasts, the Directors have reasonable expectations, as at the date of approving the financial statements, that the Group will have adequate resources to fund activities for at least twelve months from the date of the approval of the financial statements. Although the business continued to make losses throughout the year to 31 December 2022, the Company and Group have sufficient funds, contracted revenue and expected R&D tax receipts to support a cash runway to Q4 2024. This is further discussed in the financial statements.

Outlook

Subject to the top-line results of our BEN-2293 asset in an adaptive Phase I/II clinical study (expected in Q1 2023), we aim to out-license this asset in the second half of 2023. In addition, we also aim to sign an additional commercial collaboration in 2023. We anticipate that this additional capital will extend our cash runway beyond the guided Q4 2024 runway, which excludes revenues from unsigned out-licensing or collaboration agreements. In 2023, prioritisation of clinical programme spend will support our asset BEN-8744, which will enter a Phase I study in the first half of 2023. We will also invest in BEN-28010 with the aim of filing a CTA in H2 2023 for GBM, advance assets within our broader pipeline and bring new named drug programmes into the pipeline. The Company will continue to invest in the Benevolent Platform™ to increase the understanding of underlying disease biology, power the development of our in-house pipeline, and support collaborations.

Principal risks facing the business

BenevolentAI operates an embedded risk management framework, which is monitored and reviewed by the Board. There are a number of potential risks and uncertainties that could have a material impact on the Group’s financial performance and position. These include risks relating to the development of our drug portfolio and ability to out-license, the commercialisation of our technologies through collaboration, the biotech funding environment, the political environment, competitive threat, supply chain disruption, legal and regulatory, IT systems and infrastructure, cyber and data security, foreign exchange, people, COVID-19, strategic acquisitions, and the environment and climate change. These risks and the Group’s mitigating actions are set out within the Annual Report 2022.

Nicholas Keher

Chief Financial Office

1. Non-normalised expenses are defined as those related to the business combination which took place on 22 April 2022 (the “Transaction”, accounted for as a capital reorganisation); the impairment of assets or revaluation of investments for which BAI does not manage directly; and the revaluation of the warrants. See note 2.4.

2. Employee-related SBP restatement as detailed in note 28.4.

No dividend has been declared or paid in either reporting period.

The notes form an integral part of these statements.

UNAUDITED CONSOLIDATED STATEMENT OF FINANCIAL POSITION

as at 31 December 2022

. SBP restatement as detailed in note 28.4.

The notes form an integral part of these statements.

These consolidated financial statements were authorised by the Board of Directors on [20 March 2023].

UNAUDITED CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

for the year ended 31 December 2022

1. SBP restatement as detailed in note 28.4.

The notes form an integral part of these statements.

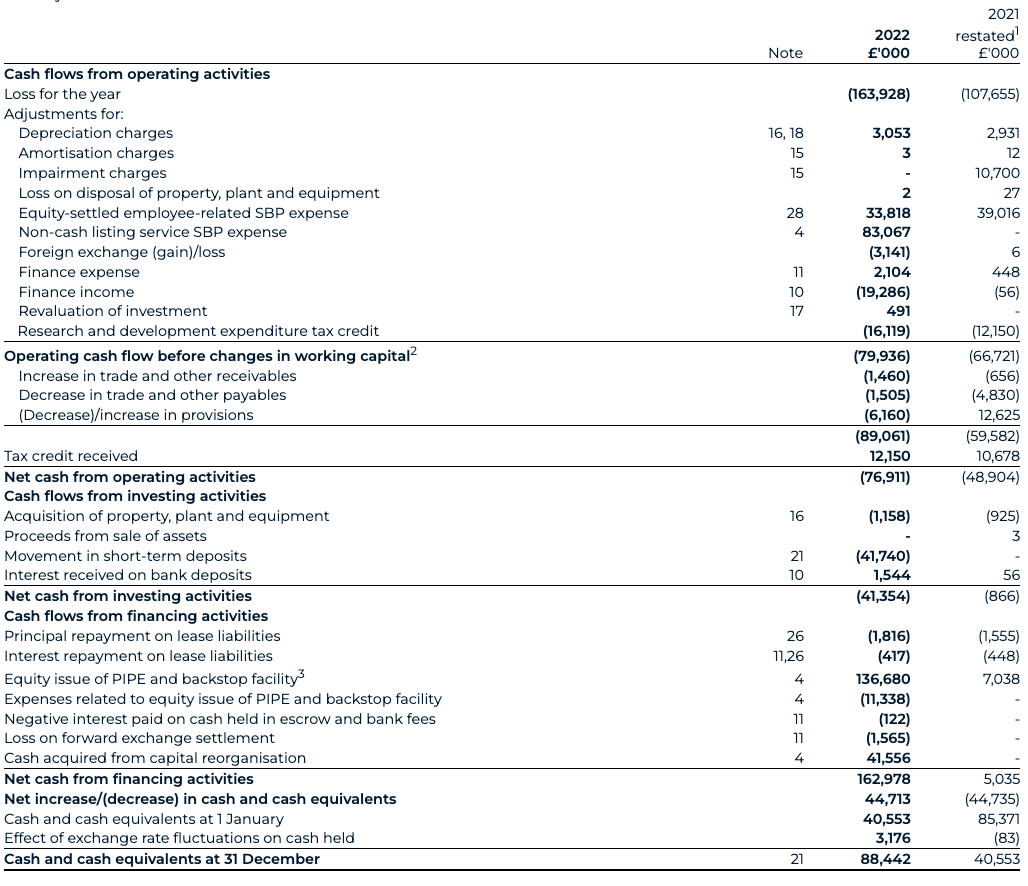

UNAUDITED CONSOLIDATED STATEMENT OF CASH FLOWS

for the year ended 31 December 2022

1. SBP restatement as detailed in note 28.4.

2. Changes in working capital for 2022 include the movement to the net assets acquired under the Transaction with Odyssey on 22 April 2022.

3. The £136.7m excludes £9.5m of non-cash consideration included in total proceeds of £146.2m.

The notes form an integral part of these statements.

UNAUDITED NOTES TO THE FINANCIAL INFORMATION

1 Background to the Group

1.1 Corporate information

BenevolentAI (the “Company”), which is a Société Anonyme, is a publicly listed company on the Euronext Amsterdam, with the ticker symbol BAI.

The Company is limited by shares, incorporated under the laws of Luxembourg under registered number B255412, having its registered office 9, rue de Bitbourg, L-273 Luxembourg, Grand Duchy of Luxembourg.

The principal activity of the Company and its subsidiaries (collectively, the “Group” or “BAI Group”) is that of creating and applying AI and machine learning to transform the way medicines are discovered and developed.

1.2 Group structure

BenevolentAI was originally known as Odyssey Acquisition S.A. (“Odyssey”), a Special Purpose Acquisition Company established for the purpose of acquiring a business with principal business operations in Europe or in another geographic area, that is based in the healthcare sector or the TMT (technology, media, telecom) sector or any other sectors. Odyssey was listed on the Euronext Amsterdam stock exchange on 6 July 2021.

On 22 April 2022 (“Closing date”), Odyssey and BenevolentAI Limited (“BAI Ltd”), the former parent company of the privately held UK group before the capital reorganisation (“Transaction”), entered into a capital reorganisation agreement by way of contribution of all shares in BAI Ltd into Odyssey in exchange for Odyssey issuing new ordinary shares. The Transaction was completed on 22 April 2022 and the name of the ultimate holding company was changed from Odyssey Acquisition S.A. to BenevolentAI, whose consolidated Group post-Transaction is referred to as BAI Group.

BAI Group is managed by its ultimate parent company BenevolentAI, with the following 5 trading subsidiaries operating under one segment. The Group’s opportunity to deliver future value depends on a unified and amalgamated approach across the whole of the Group and could not be achieved independently by any individual entity or separately identifiable line of business.

|

1. Held indirectly |

||||

|

2. The country of registration for each subsidiary is also its principal place of business |

2 Accounting policies

2.1 Basis of preparation

The Group’s consolidated financial statements for the year ended 31 December 2022 have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as adopted by the EU, and applicable law. They have been prepared on a historical cost basis, except for financial instruments measured at fair value, and all amounts have been rounded to the nearest £‘000. As set out in note 2.2 below, the Group financial statements have been prepared on a going concern basis.

The accounting policies set out below have, unless otherwise stated, been applied consistently to all periods presented in these financial statements. Judgements made by the directors in the application of these accounting policies that have significant effect on the financial statements and estimates with a significant risk of material adjustment in the next year are discussed in note 3.

No new standards have been early adopted by the Group in the year. A number of new standards are effective for annual periods beginning on or after 1 January 2023 and earlier application is permitted; however, the Group has not early adopted the new or amended standards in preparing these consolidated financial statements.

The following new and amended standards are not expected to have a significant impact on the Group’s consolidated financial statements.

- IFRS 17 Insurance Contracts (issued on 18 May 2017; including Amendments to IFRS 17) and Initial Application of IFRS 17 and IFRS 9 Comparative information (issued after 25 June 2021)

- Amendments to IAS 8 Accounting policies, Changes in Accounting Estimates and Errors: Definition of Accounting Estimates (issued on 12 February 2021)

- Amendments to IFRS 16 Leases on sale and leaseback: These amendments include requirements for sale and leaseback transactions in IFRS 16 to explain how an entity accounts for a sale and leaseback after the date of the transaction (issued on 22 September 2022)

- Amendments to IAS 1, Non-current liabilities with covenants: These amendments clarify how conditions with which an entity must comply within twelve months after the reporting period affect the classification of a liability (issued on 31 October 2022)

- Amendments to IAS 1, aim to improve accounting policy disclosures and to help users of the financial statements to distinguish between changes in accounting estimates and changes in accounting policies.

- Amendments to IAS 12 Income Taxes: Deferred Tax related to Assets and Liabilities arising from a Single Transaction (issued on 7 May 2021)

2.2 Going concern

The financial statements have been prepared on the going concern basis, which the Directors consider appropriate for the following reasons.

Cash flow forecasts have been prepared for a period in excess of 12 months from the date of approval of these financial statements (the going concern period). These forecasts include a base case scenario, which excludes any unsigned revenue contracts. Additionally, severe but plausible downside scenarios have also been considered, with corresponding mitigating actions that allow for an extension of the Group's cash runway.

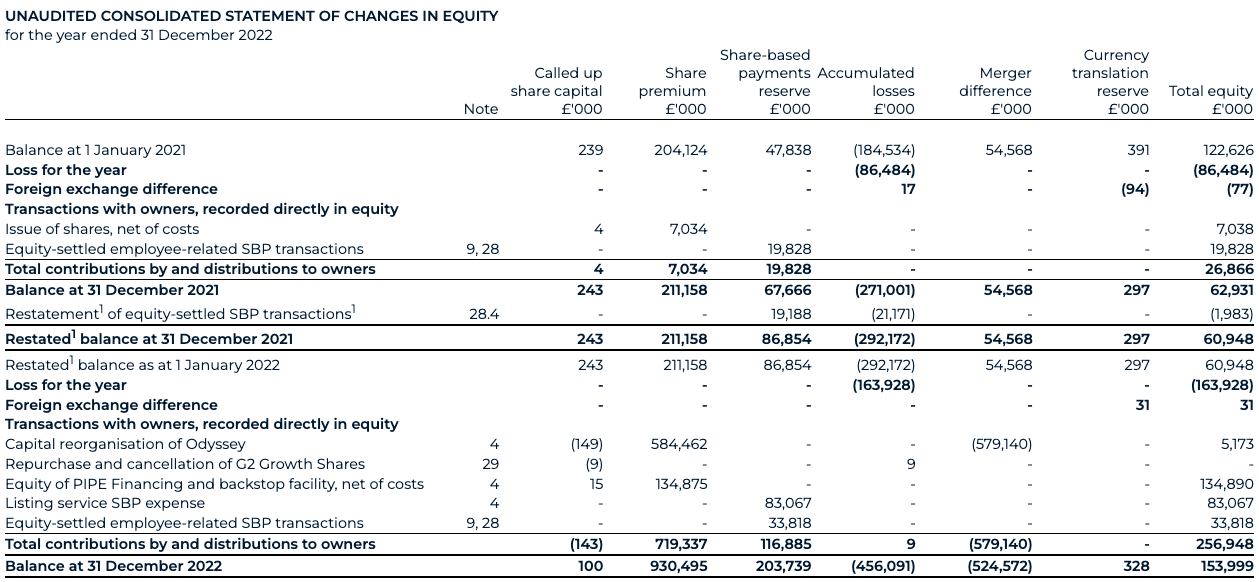

The Group’s cash, cash equivalents and short-term deposits position of £130.2m (2021: £40.6m) comes largely from issuing equity, most recently from the business combination completed in April 2022 (see note 4) and related equity PIPE investment. The base case scenario includes a substantial cash position held by the Group and excludes unsigned revenue which could be secured as part of normal operating activities.

The severe but plausible scenario downside scenarios consider the Group’s exposure to macroeconomic factors, including inflation, tax credit regime changes and supply chain risk. No combination of these factors indicates that additional funding will be needed throughout the going concern period, due to various mitigating actions that the Directors could implement to preserve cash if needed. These mitigating actions include a reduction in operating expenses (which are within the control of the Directors). These forecasts indicate that the Group will have sufficient funds to meet its liabilities for the going concern period.

The Group continues to rely on equity to fund its operations in the medium to long term. The Directors remain confident that, when it is required, such further funding will be accessible to the Group.

As a result, the Directors are confident that the Group will have sufficient funds to continue to meet its liabilities as they fall due for at least 12 months from the date of approval of these financial statements and have therefore prepared the financial statements on a going concern basis.

2.3 Basis of consolidation

Subsidiaries

Subsidiaries are entities controlled by the Group. The Group controls an entity when it is exposed to, or has rights to, variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity. In assessing control, the Group takes into consideration potential voting rights that are currently exercisable. The acquisition date is the date on which control is transferred to the acquirer. The financial statements of subsidiaries are included in the consolidated financial statements from the date that control commences until the date that control ceases. Losses applicable to the non-controlling interests in a subsidiary are allocated to the non-controlling interests even if doing so causes the non-controlling interests to have a deficit balance.

Transactions eliminated on consolidation

Intra-group balances and transactions, and any unrealised income and expenses arising from intra-group transactions, are eliminated.

2.4 Normalised operating loss and cash flows

Normalised operating loss for the years ended 31 December 2022 and 31 December 2021 is defined as operating loss excluding non-normalised transactions, defined as those related to the business combination; the impairment of assets or revaluation of investments for which BAI does manage directly; and the revaluation of the warrants recognised as finance income. This is to show an underlying representation of operating losses for the respective periods and extends to normalised operating cash flows on the same basis.

Normalised operating losses, normalised operating cash flows and non-normalised transactions are each alternative performance measures (“APMs”) that are not calculated in accordance with IFRS and, therefore, may not be directly comparable with other companies’ APMs, including those in the Group’s industry. APMs should be considered in addition to, and are not intended to substitute or supersede, IFRS measures.

This APM is in our view an important metric for a biotech company in the development stage. Removing the non-normalised costs, given their material, isolated and one-off nature, enables users to better compare the Group’s normal operating performance between reporting periods.

The following table presents a reconciliation of normalised operating loss, to the closest IFRS measures, for the year ended 31 December:

Similarly, normalised operating cash flows are considered on the same basis and to the same effect. The following table presents a reconciliation to the closest IFRS measures for the year ended 31 December:

2.5 Change in functional currency of BenevolentAI

As of 22 April 2022, management reviewed the functional currency of BenevolentAI and the presentation currency of the Group. The change in functional currency for standalone BenevolentAI was made, from euros (“EUR”) to pound sterling (“GBP”) to reflect that GBP has become the predominant operating currency for the Company representing a significant part of its cash flows and its operating environment, while the Group presentation currency remains in GBP consistent with the prior year.

The Group presents as comparative information the financial information of the former BenevolentAI Limited Group, which had GBP as its functional and presentation currency. That is, as discussed in note 2.14, the new Group’s consolidated statement of comprehensive income contains only the post-acquisition performance of BenevolentAI. Comparative information, therefore, has not been re-stated following this change to BenevolentAI’s functional currency.

2.6 Foreign currency

Transactions in foreign currencies are translated to the respective functional currencies of Group entities at the foreign exchange rate ruling at the date of the transaction. Monetary assets and liabilities denominated in foreign currencies at the balance sheet date are retranslated to the functional currency at the foreign exchange rate ruling at that date. Foreign exchange differences arising on translation are recognised in the consolidated statement of comprehensive income. Non-monetary assets and liabilities that are measured in terms of historical cost in a foreign currency are translated using the exchange rate at the date of the transaction. Non-monetary assets and liabilities denominated in foreign currencies that are stated at fair value are retranslated to the functional currency at foreign exchange rates ruling at the dates the fair value was determined.

The assets and liabilities of foreign operations, including goodwill and fair value adjustments arising on consolidation, are translated to the Group’s presentational currency, GBP, at foreign exchange rates ruling at the balance sheet date. The revenues and expenses of foreign operations are translated at an average rate for the year where this rate approximates to the foreign exchange rates ruling at the dates of the transactions.

Exchange differences arising from this translation of foreign operations are reported as an item of other comprehensive income and accumulated in the translation reserve. When a foreign operation is disposed of, such that control, or significant influence (as the case may be) is lost, the entire accumulated amount in the foreign currency translation reserve, is recycled to profit or loss as part of the gain or loss on disposal.

2.7 Classification of financial instruments issued by the Company

Following the adoption of IAS 32, financial instruments issued by the Company are treated as equity only to the extent that they meet the following two conditions:

(a) they include no contractual obligations upon the Company to deliver cash or other financial assets or to exchange financial assets or financial liabilities with another party under conditions that are potentially unfavourable to the Company; and

(b) where the instrument will or may be settled in the Company’s own equity instruments, it is either a non-derivative that includes no obligation to deliver a variable number of the Company’s own equity instruments or is a derivative that will be settled by the Company’s exchanging a fixed amount of cash or other financial assets for a fixed number of its own equity instruments.

To the extent that this definition is not met, the proceeds of issue are classified as a financial liability. Where the instrument so classified takes the legal form of the Company’s own shares, the amounts presented in these consolidated financial statements for called up share capital and share premium account exclude amounts in relation to those shares.

2.8 Non-derivative financial instruments

Non-derivative financial instruments comprise investments in equity, trade and other receivables, cash and cash equivalents, and trade and other payables.

Trade and other receivables

Trade and other receivables are recognised initially at fair value. Subsequent to initial recognition they are measured at amortised cost using the effective interest method, less any expected credit losses (“ECLs”).

Trade and other payables

Trade and other payables are recognised initially at fair value. Subsequent to initial recognition they are measured at amortised cost using the effective interest method.

Cash and cash equivalents

Cash and cash equivalents include cash balances and cash deposits with maturities of less than 3 months at their inception

Short-term deposits

Short-term deposits include cash deposits with maturities of greater than 3 months but less than 12 months at their inception.

Investments

Investments are recognised initially at fair value. Subsequent to the initial recognition they are measured at fair value through profit or loss using latest observable share price.

2.9 Derivative financial instruments

Warrants

As part of the Business Combination transaction, BAI Group took on warrants which had been initially issued by Odyssey prior to the Transaction, as part of financing Odyssey’s working capital and investment.

A derivative, other than a derivative that meets the definition of an equity instrument, is initially recognised as a financial asset or financial liability at its fair value on the date the derivative contract is entered into, and the related transaction costs are expensed. The fair values of the derivatives are remeasured at the end of each reporting period with changes in fair values recognised through profit or loss.

A derivative that will be settled by the Company delivering a fixed number of its own equity instruments in exchange for a fixed amount of cash in terms of its functional currency or another financial asset is classified and presented as an equity instrument, rather than a financial liability. As the exercise price of the Company’s share purchase warrants that are exercisable into common shares is denominated in EUR, however, the Company will receive a variable amount of cash in terms of its GBP functional currency upon exercise of the warrants due to movements in foreign exchange.

The warrants are, therefore, presented as derivative financial liabilities.

Monetary assets and liabilities denominated in foreign currencies at the balance sheet date are retranslated to the functional currency at the foreign exchange rate ruling at that date. Foreign exchange differences arising on translation of the EUR denominated warrants are recognised as finance income/expense in the consolidated statement of comprehensive income.

2.10 Intangible assets

Goodwill

Goodwill is stated at cost less any accumulated impairment losses. Goodwill is allocated to a single identifiable cash-generating unit and is not amortised but instead tested annually for impairment.

Research and development

Expenditure on research activities is recognised in the consolidated statement of comprehensive income as an expense as incurred.

Expenditure on development activities is capitalised if the product or process is technically and commercially feasible and the Group intends and has the technical ability and sufficient resources to complete development, future economic benefits are probable and if the Group can measure reliably the expenditure attributable to the intangible asset during its development. Development activities involve a plan or design for the production of new or substantially improved products or processes. The expenditure capitalised includes the cost of materials, direct labour and an appropriate proportion of overheads and capitalised borrowing costs. Other development expenditure is recognised in the consolidated statement of comprehensive income as an expense as incurred. Capitalised development expenditure is stated at cost less accumulated amortisation and less accumulated impairment losses.

Other Intangible assets

Expenditure on internally generated goodwill and brands is recognised in the consolidated statement of comprehensive income as an expense as incurred.

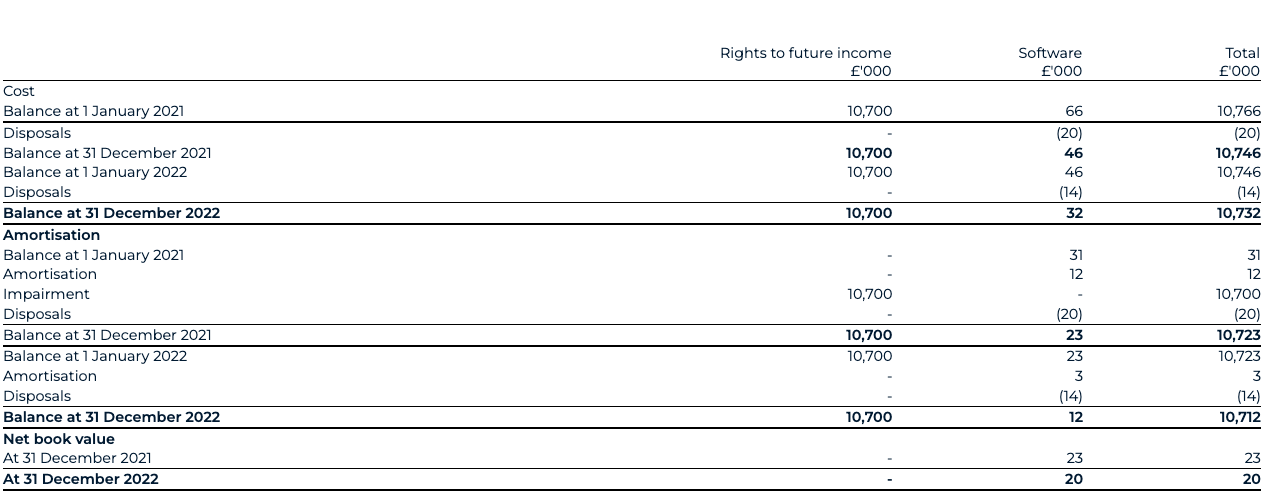

Patents or rights to their future income acquired by the Company are initially recognised based on transaction price and stated at this cost less accumulated amortisation. Indicators of impairment are assessed at the end of each reporting period.

Other intangible assets that are acquired by the Company are stated at cost less accumulated amortisation and less accumulated impairment losses.

Amortisation

Amortisation is recognised as an administrative expense in the consolidated statement of comprehensive income on a straight-line basis over the estimated useful lives of intangible assets, starting from the date they are available for use. The estimated useful life and amortisation method are reviewed at the end of each reporting period, with the effect of any changes in estimate being accounted for on a prospective basis. The estimated useful lives are as follows:

- Patents or rights to their future income – over the expected duration of the patent

- Software - length of software licence

Goodwill and intangible assets with an indefinite useful life are not amortised but are systematically tested for impairment annually.

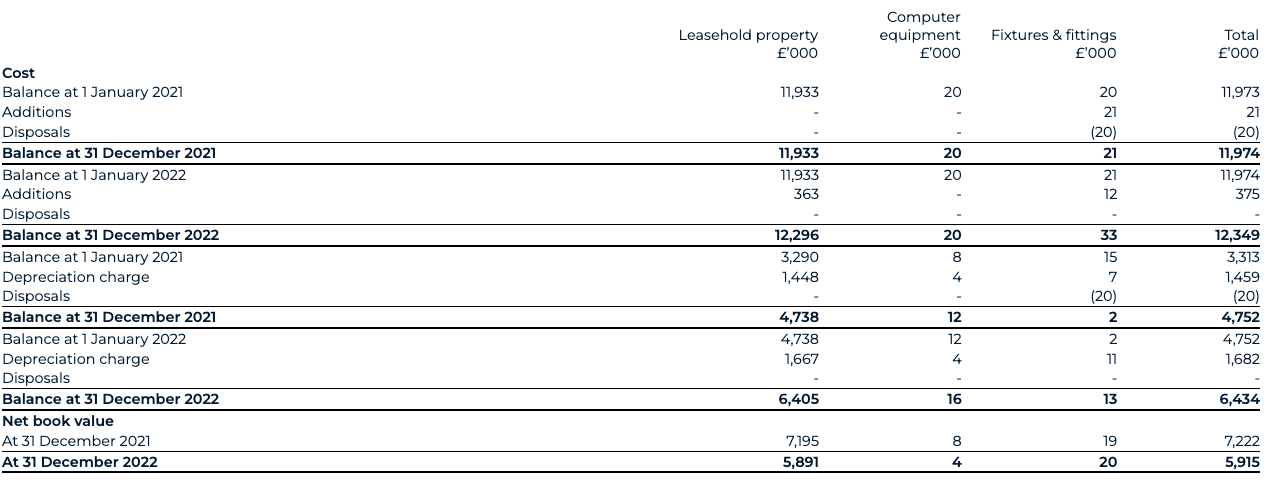

2.11 Property, plant and equipment

Property, plant and equipment are stated at cost less accumulated depreciation and accumulated impairment losses.

Where parts of an item of property, plant and equipment have different useful lives, they are accounted for as separate items of property, plant and equipment.

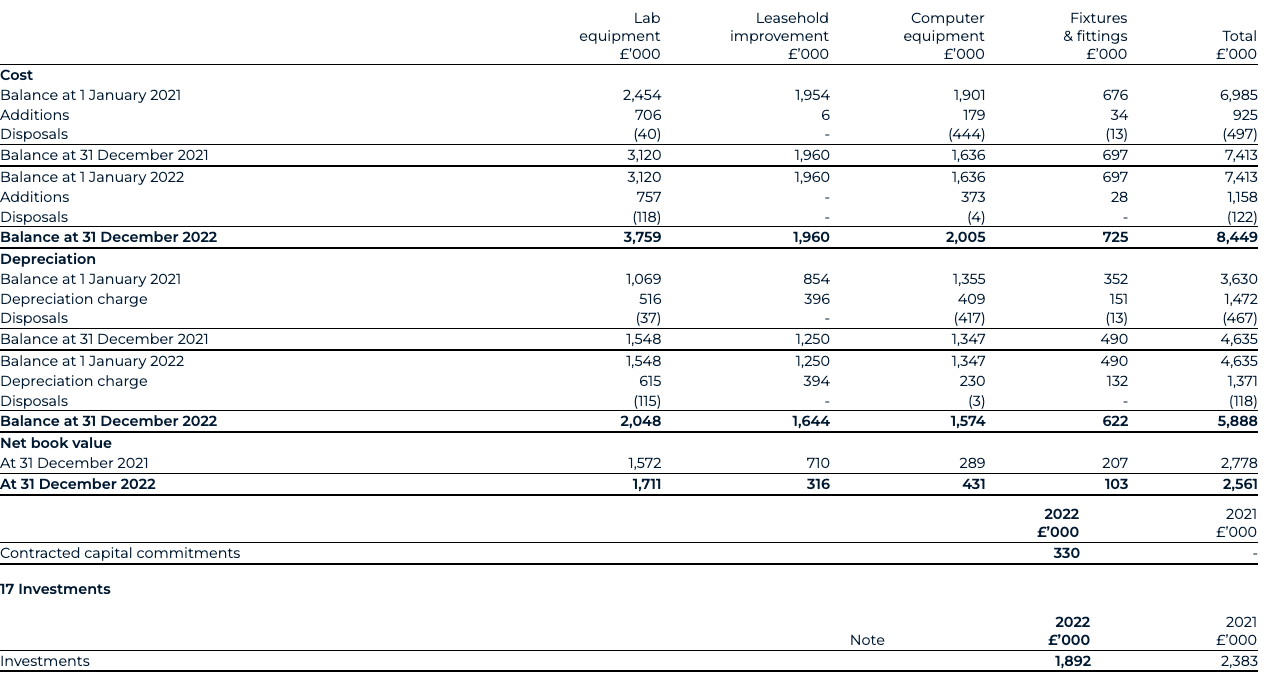

Depreciation is charged to the consolidated statement of comprehensive income under either the administrative expense or R&D expense, depending on the classification of the asset, on a straight-line basis over the estimated useful lives of each part of an item of tangible fixed assets. Leased assets are depreciated over the shorter of the lease term and their useful lives. The estimated useful lives are as follows:

- laboratory equipment 4 - 10 years

- computer equipment 3 years

- fixtures and fittings 4 - 5 years

- leasehold improvements life of the lease

Depreciation methods, useful lives and residual values are reviewed if there is an indication of a significant change since last annual reporting date in the pattern by which the Company expects to consume an asset’s future economic benefits.

2.12 Right-of-use assets

A right-of-use asset is recognised at the commencement date of a lease. The right-of-use asset is measured at cost, which comprises the initial amount of the lease liability, adjusted for, as applicable, any lease payments made at or before the commencement date net of any lease incentives received, any initial direct costs incurred and an estimate of costs expected to be incurred for dismantling and removing the underlying asset, and restoring the site or asset.

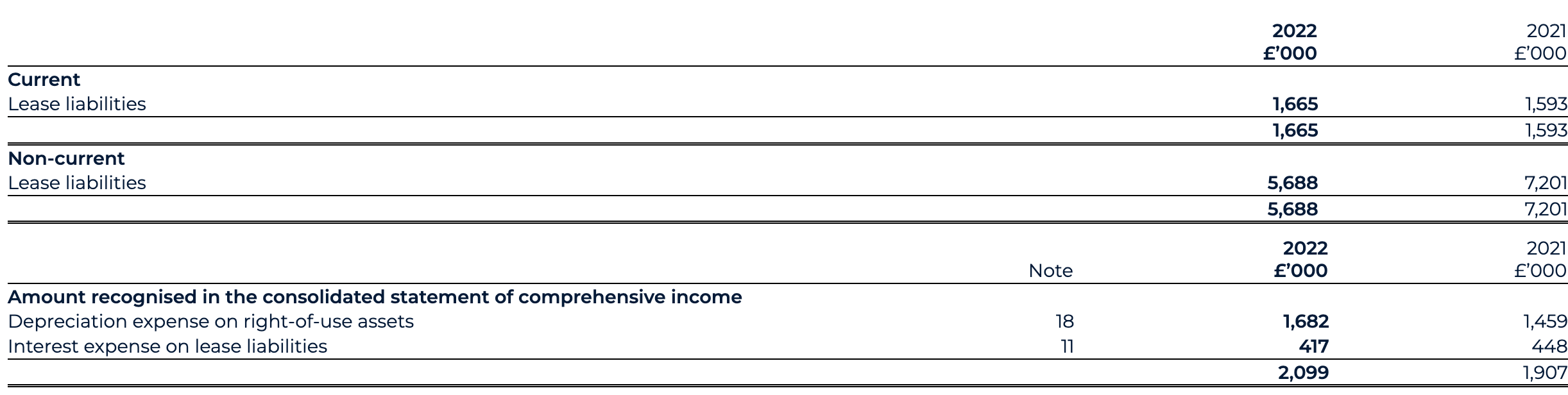

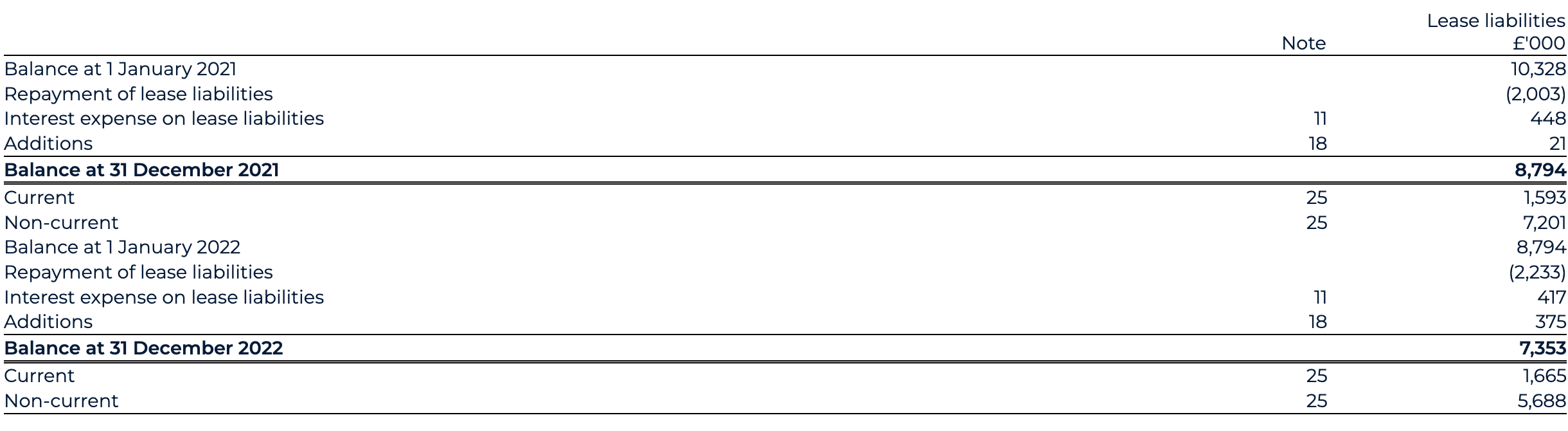

Right-of-use assets are depreciated on a straight-line basis over the unexpired period of the lease or the estimated useful life of the asset, whichever is the shorter. Where the Company expects to obtain ownership of the leased asset at the end of the lease term, the depreciation is over its estimated useful life. Right-of-use assets are subject to impairment or adjusted for any remeasurement of lease liabilities.

The Company has elected not to recognise a right-of-use asset and corresponding lease liability for short-term leases with terms of 12 months or less and leases of low-value assets. Lease payments on these assets are expensed to profit or loss as incurred.

2.13 Business combinations

Business combinations are accounted for using the acquisition method as at the acquisition date, which is the date on which control is transferred to the Group.

The Group measures goodwill at the acquisition date as:

- the fair value of the consideration transferred; plus

- the recognised amount of any non-controlling interests in the acquiree; plus

- the fair value of the existing equity interest in the acquiree; less

- the net recognised amount (generally fair value) of the identifiable assets acquired and liabilities assumed.

Any contingent consideration payable is recognised at fair value at the acquisition date. If the contingent consideration is classified as equity, it is not remeasured, and settlement is accounted for within equity. Otherwise, subsequent changes to the fair value of the contingent consideration are recognised in profit or loss.

2.14 Capital reorganisation

The business combination between BAI Ltd and Odyssey is accounted for within the scope of IFRS 2 as a capital reorganisation since Odyssey did not meet the definition of a business in accordance with IFRS 3. Under this accounting method, Odyssey is treated as the acquired company for financial reporting purposes.

Accordingly, for financial reporting purposes, the Transaction was treated as the equivalent of BAI Ltd issuing shares at the closing of the Business Combination for the net assets of Odyssey as at the Closing date. The capital reorganisation reflects the transition of the share capital and share premium from BAI Ltd to BenevolentAI, which comprises the legal essence of the Transaction. This results in a decrease within share capital and related increase to share premium, to align the equity of BAI Ltd (as the acquirer for financial reporting purposes) with the equity of the Group’s new ultimate legal parent, BenevolentAI. The book value accounted for on consolidation is reflected through a corresponding charge to merger difference, such that the net impact to equity is equal to the net assets acquired (£5.2m, see note 4).

The excess of the fair value of consideration for Odyssey over the fair value of its identifiable net assets acquired represents a compensation for the service of a stock exchange listing for its shares and expenses as incurred.

The comparatives in the financial statements represent the financial information of BAI Ltd and its subsidiaries, both to 31 December 2021 and as at 31 December 2021. The activity and position of the acquired Odyssey is considered only from the Closing date onwards. That is, the consolidated statement of comprehensive income contains only the post-acquisition performance of BenevolentAI. See note 4 for further details.

2.15 Impairment

Financial assets (including receivables)

Financial assets are assessed for indicators of impairment at the end of the reporting period. The Group recognises an allowance for expected credit losses (“ECLs") for all debt instruments not held at fair value through profit or loss. ECLs are based on the difference between the contractual cash flows due in accordance with the contract and all the cash flows that the company expects to receive, discounted at an approximation of the original effective interest rate.

For credit exposures for which there has not been a significant increase in credit risk since initial recognition, ECLs are provided for credit losses that result from default events that are possible within the next twelve months. For those credit exposures for which there has been a significant increase in credit risk since initial recognition, a loss allowance is required for credit losses expected over the remaining life of the exposure, irrespective of the timing of the default.

Non-financial assets

The carrying amounts of the Company’s non-financial assets are reviewed at each reporting date to determine whether there is any indication of impairment. If any such indication exists, then the asset’s recoverable amount is estimated.

The recoverable amount of an asset or cash-generating unit (“CGU”) is the greater of its value in use and its fair value less costs to sell. Goodwill acquired in a business combination is allocated to groups of CGUs that are expected to benefit from the synergies of the combination. In assessing the fair value of the CGU, we have considered quoted market prices in an active market, as we consider the Group as a single CGU. For the purpose of impairment testing, assets that cannot be tested individually are grouped together into the smallest group of assets that generates cash inflows from continuing use that are largely independent of the cash inflows of other assets or groups of assets (the CGU).

An impairment loss is recognised if the carrying amount of an asset or its CGU exceeds its estimated recoverable amount. Impairment losses are recognised in profit or loss. Impairment losses recognised in respect of CGUs are allocated first to reduce the carrying amount of any goodwill allocated to the units, and then to reduce the carrying amounts of the other assets in the unit (group of units) on a pro rata basis.

An impairment loss in respect of goodwill is not reversed. In respect of other assets, impairment losses recognised in prior periods are assessed at each reporting date for any indications that the loss has decreased or no longer exists. An impairment loss is reversed if there has been a change in the estimates used to determine the recoverable amount. An impairment loss is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortisation, if no impairment loss had been recognised.

2.16 Employee benefits

Defined contribution plans

A defined contribution plan is a post-employment benefit plan under which the Company pays fixed contributions into a separate entity and will have no legal or constructive obligation to pay further amounts. Obligations for contributions to defined contribution pension plans are recognised as an expense in the consolidated statement of comprehensive income in the periods during which services are rendered by employees.

Share-based payment transactions – BenevolentAI Equity Incentive Scheme (“BEIS”)

Share-based payment arrangements in which the Group receives goods or services as consideration for its own equity instruments are accounted for as equity-settled share-based payment transactions, regardless of how the equity instruments are obtained by the Group.

Options or restricted stock units (“RSUs”) granted under the BEIS are comprised of tranches that represent each increment that participants become entitled to over the vesting period. The fair value of each of these vesting tranches is recognised as an employee or related expense in the consolidated statement of comprehensive income, on a straight-line basis over the longer of either the time until the service condition is met or the trigger event is expected to take place (“vesting period”), with a corresponding movement to equity reserves. For each tranche continuing to have their FV charged after the trigger event, this is spread on a straight line basis over the service period. The fair value of the awards granted is measured using the Black-Scholes model. The amount to be expensed over the vesting period is adjusted to reflect the number of awards for which the related non-market vesting conditions are expected to be met, such that the amount ultimately recognised as an expense is based on the number of awards that meet the related non-market performance conditions at the vesting date.

At each consolidated statement of financial position date, the Group revises its estimates of the number of awards that are expected to vest, as well as the estimate of the vesting period. The impact of the revisions of original estimates, if any, is recognised in the consolidated statement of comprehensive income, with a corresponding adjustment to equity reserves, over the remaining vesting period.

Share-based payment transactions – Long Term Incentive Plan (“LTIP”)

Awards granted to participants under the LTIP comprise of RSUs and performance stock units (“PSUs”). The fair value for the RSUs has been determined and recognised on the same basis as under the BEIS post trigger event, namely tied to the service condition.

The PSUs include both non-market vesting conditions and market vesting conditions. As with the BEIS, the number of equity instruments expected to vest which are tied to the non-market conditions is revisited at each balance sheet date so that, ultimately, the cumulative amount recognised over the vesting period is based on the number of instruments that eventually vest.

Market vesting conditions, however, are factored into the fair value of the awards granted. The portion of each PSU which relates to market vesting conditions carries a separate fair value, determined using the Monte Carlo Simulation model. Provided all other vesting conditions are satisfied, a charge is made irrespective of whether the market vesting conditions are satisfied. The cumulative expense is not adjusted for failure to achieve a market vesting condition.

Tax payments related to share-based payments

Historically, the liability arising from any tax due in any jurisdiction in relation to equity compensation sat with the beneficiary of that instrument. Following a board resolution and subsequent communication to employees in the second half of 2021, the tax liability has been transferred to the Group.

This liability is recognised in-line with the relative portion of fair value charged for each tranche as at the balance sheet date, under both the BEIS and LTIP, adjusted for changes in expectation with regards to the non-market vesting conditions and based on the latest market share price available as at that same date.

2.17 Revenue recognition

The Group’s revenue is generated from licence or collaboration agreements.

Collaboration agreements typically have an initial upfront payment, periodic collaboration payments and potential milestone payments for research, development and commercial achievements plus royalties on net sales. We initially recognise income under the collaboration as deferred revenue, which we become entitled to reclassify as revenue in line with the completion of performance obligations, measured as a percentage complete against the latest collaboration team forecasts.

When the Group receives milestone payments for achieving pre-defined targets during pre-clinical and clinical development, these milestones are recognised when probable (i.e. on achievement of the pre-defined target). except where the milestone or a proportion of the milestone is to be applied to the development of the programme which is the subject of the collaboration agreement. In such circumstances, the income is deferred and recognised as income by reference to the development costs incurred in developing the programme towards the next milestone.

The rules for revenue recognition are stipulated by the accounting standard IFRS 15 which we have adopted in these consolidated financial statements.

2.18 Other income

The group recognises income for all government grants in relation to research and development, where there is reasonable assurance that the grant will be received and attached conditions will be complied with.

2.19 Expenses

Operating lease

Payments (excluding costs for services and insurance) made under operating leases are recognised in the profit and loss account on a straight-line basis over the term of the lease where these are short-term leases with a period remaining of less than 12 months or for low value. Other leases that are assessed under IFRS 16 as finance leases have been accounted for in accordance with IFRS.

Research & development (“R&D”) expenditure

R&D expenditure, which includes a proportion of staff costs and directly attributable overheads, is currently recognised in the consolidated statement of comprehensive income as incurred, on the basis that the recognition criteria of IAS 38 (Intangible Assets) are currently not met.

2.20 Interest income and expenditure

Interest income and expenditure is recognised in the consolidated statement of comprehensive income as it accrues on a timely basis, by reference to the principal outstanding and effective interest rate applicable. Other finance income and expenditure relates to the fair value revaluation of the warrant liabilities at the balance sheet date, as well as the settlement of forward contracts.

2.21 Taxation

Tax on the profit or loss for the year comprises current and deferred tax. Tax is recognised in the consolidated statement of comprehensive income except to the extent that it relates to items recognised directly in equity, in which case it is recognised in equity.

Current tax is the expected tax payable or receivable on the taxable income or loss for the year, using tax rates enacted or substantively enacted at the balance sheet date, and any adjustment to tax payable in respect of previous years.

Deferred tax is provided on temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. The following temporary differences are not provided for: the initial recognition of goodwill; the initial recognition of assets or liabilities that affect neither accounting nor taxable profit other than in a business combination, and differences relating to investments in subsidiaries to the extent that they will probably not reverse in the foreseeable future. The amount of deferred tax provided is based on the expected manner of realisation or settlement of the carrying amount of assets and liabilities, using tax rates enacted or substantively enacted at the balance sheet date.

A deferred tax asset is recognised only to the extent that it is probable that future taxable profits will be available against which the temporary difference can be utilised.

2.22 Issued capital

Ordinary, preference and growth shares are classified as equity. Proceeds in excess of the par value of the shares are shown as share premium in equity and incremental costs directly attributable to the issue of new shares or options are shown in equity as a deduction of share premium, net of tax, from the proceeds.

2.23 Provisions

A provision is recognised in the balance sheet when the Group has a present legal or constructive obligation as a result of a past event, that can be reliably measured and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects risks specific to the liability, where this would be material.

3 Critical accounting judgements and key sources of estimation uncertainty

Judgements and estimates are continually evaluated and are based on historical experience and other relevant factors, including management’s reasonable expectations of future events. The preparation of these consolidated financial statements requires management to make estimates and assumptions concerning the future. The estimates and the underlying assumptions are subject to continuous review.

The Group based its assumptions and estimates on parameters available when the financial statements were prepared. Existing circumstances and assumptions about future developments, however, may change due to market changes or circumstances arising that are beyond the control of the Group. Such changes are reflected in the assumptions when they occur.

In preparing these consolidated financial statements, the significant judgements made by management in applying the Group’s accounting policies and the key sources of estimation uncertainty are as follows.

3.1 Critical judgements in applying accounting policies

Revenue

In the year, the Group entered a second collaboration agreement with AstraZeneca (“AZ”). The new collaboration is related to two new disease areas and has been treated by the Group as a separate agreement, since it has identified new and distinct performance obligations that did not exist in the previous agreement entered in 2021.

The Group’s main collaboration works across two disease areas using a similar methodology in each. In identifying the performance obligations within the contract, management has made judgements in categorizing each disease area as its own discrete performance obligation, where their delivery is both independent from one another and deemed to require an equal amount of effort, and where they are individually considered a distinct bundle of services.

Goodwill and Intangible Assets

The amount of goodwill and intangible assets initially recognised as a result of a business combination is dependent on the allocation of the purchase price to the fair value of the identifiable assets acquired and the liabilities assumed.

The determination of the fair value of the assets and liabilities is based, to a considerable extent, on management’s judgement and on industry benchmarks and information relevant to the specific assets in focus. The carrying value of the goodwill is in line with the allocation of the purchase price in 2018, arising from the acquisition of BenevolentAI Cambridge Limited.

During 2022, management has performed an impairment assessment on the goodwill in accordance with IAS 36. For the purposes of impairment assessment, goodwill has been allocated to the Group’s CGU defined as the whole of the BenevolentAI Group (BAI Group). CGU is the smallest identifiable group of assets that generates cash inflows that are largely independent of the cash inflows from other assets. Management, as part of their continued evaluation of the goodwill, has considered that the CGU for 2022 is the BAI Group, since Management has now considered that the assets held by BenevolentAI Cambridge Limited is now, and increasingly so, strategically integrated with the other legal entities in the Group. By this very nature Management believes for any future commercial value created through the current and future drug programs, then a unified and amalgamated approach is required across the whole of the Group. In 2021 for the purposes of impairment testing, goodwill has been allocated to the Group’s CGU defined as the whole of the BenevolentAI Cambridge Limited entity.

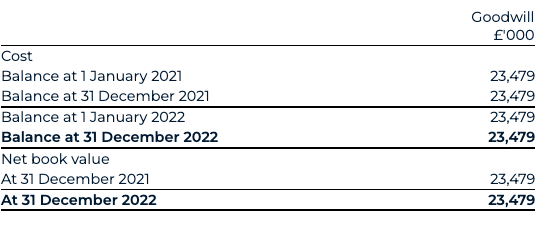

Per IAS 36.6, impairment is recognised as an expense in the consolidated statement of comprehensive income if the recoverable value (higher of fair value less cost of disposal or value in use, “FVLCTS”) of an asset is less than its carrying value. The carrying value of the goodwill which is currently held in the balance sheet as at 31 December 2022 is £23,479k.

The net recoverable amount or FVLCTS of the CGU is estimated using the Group’s quoted market value at year end. Since the Group is a listed quoted entity, the fair value can be determined by the quoted share price of BAI as at closing on 31 December 2022, which was at £3.10 per share (€3.50 per share) equivalent to an overall £364,775k fair value of the CGU. This exceeds the Group’s net assets of £153,999k inclusive of the goodwill amount, as such there are no impairment indicators to the current carrying value of the goodwill.

3.2 Other accounting estimates

The Group has not identified any significant accounting estimates, being those which present a significant risk of material adjustment in the next financial period. However, other areas of estimation uncertainty have been identified as follow:

Revenue

In recognizing revenue against the individual performance obligations, estimates have been made in the calculation of their percentage complete, the key driver of revenue release. This requires an estimation of full-time equivalent (“FTE”) days needed to fully satisfy each performance obligation.

Share-based payments charge

The Group operates the BenevolentAI Equity Incentive Scheme (“BEIS”) and long-term incentive plan (“LTIP”). The fair value of equity incentive awards, or respective portions of awards, related solely to non-market vesting conditions is measured using the Black Scholes model at each grant date. The number of equity instruments expected to vest which are tied to the non-market conditions is revisited at each balance sheet date so that, ultimately, the cumulative amount recognised over the vesting period is based on the number of instruments expected to eventually vest.

The fair value of equity incentive award portions related to market vesting conditions is measured using the Monte Carlo Simulation model at each grant date. Provided all other vesting conditions are satisfied, a charge is made irrespective of whether the market vesting conditions are satisfied.

The net increase in relative portion of fair value charge during the year is recognised in the consolidated statement of comprehensive income. The assumptions used in both the Black Scholes and Monte Carlo Simulation models are detailed in note 28.

Fair value revaluation of class A warrants and class B warrants

The Company's warrants are classified and presented as derivative financial liabilities and measured at fair value through profit or loss. The fair value of each warrant class is determined at each reporting date and exercise date and is based on quoted market prices, where available, or independently valued using the Binomial Tree method and Monte Carlo Simulation models, the inputs for which derive from significant observable market inputs (volatility, discount rate and share price).

Fair value revaluation of class A shares and class B shares

As part of the accounting impact of the business combination with Odyssey in the year, the consideration deemed to have been issued by BAI Ltd is based on the value of Odyssey shares at the Closing date. As with the warrants, the fair value of each share class was determined based on quoted market prices, where available, or independently valued using the Binomial Tree method and Monte Carlo Simulation models, the inputs for which derive from significant observable market inputs (volatility, discount rate and share price).

4 Accounting impact of the business combination

Following the successful completion of the business combination with Odyssey on 22 April 2022, BenevolentAI became the new name of the holding company of the new BAI Group.

This business combination was achieved through the contribution of ordinary and preferred shares in BAI Ltd in exchange for new ordinary shares in BenevolentAI (previously Odyssey), the result being that the new BAI Group became listed on the Euronext Amsterdam stock exchange.

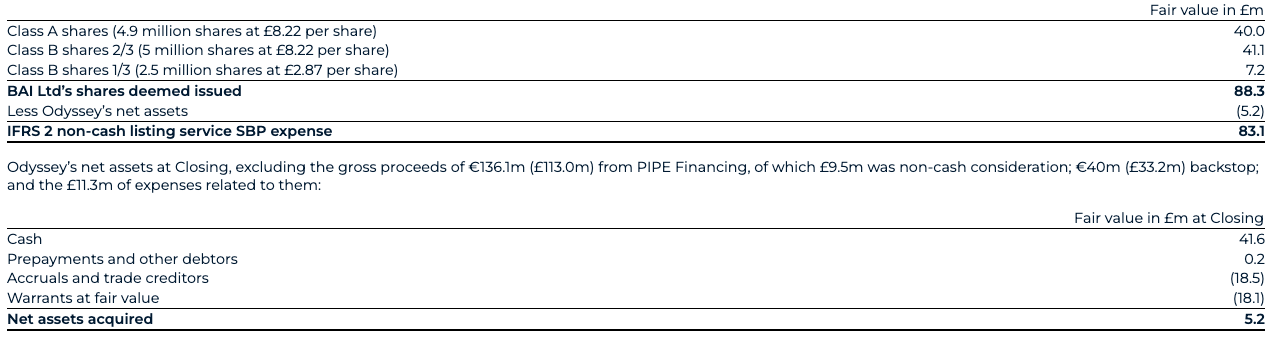

As discussed in note 2.14, the business combination between BAI Ltd and Odyssey was accounted for as a capital reorganisation under IFRS 2 (Share-based Payment). Accordingly, the Transaction was treated as the equivalent of BAI Ltd issuing shares at the closing of the business combination for the net assets of Odyssey as at the Closing date. The excess of the fair value of consideration for Odyssey over the fair value of its identifiable net assets acquired represents a compensation for the service of a stock exchange listing for its shares and expenses as incurred. This leads to a non-cash listing service SBP expense of £83.1m, determined under IFRS 2 and recognised in administrative expenses.

As at Closing date, the fair value of BAI Ltd’s shares that were deemed to be issued to Odyssey amounted to £88.3m, based on the initial closing price of shares of Odyssey according to the table below. In return, BenevolentAI received Odyssey’s listing service and its net assets, equal to £5.2m, which mainly consisted of remaining cash net of redemptions and liabilities related to the warrants, resulting in a total non-cash listing service SBP expense of £83.1m to administrative expenses.

The warrants acquired represent the fair value of the 10,000,000 class A warrants and 6,600,000 class B warrants at the Closing date, assessed using significant observable market inputs.

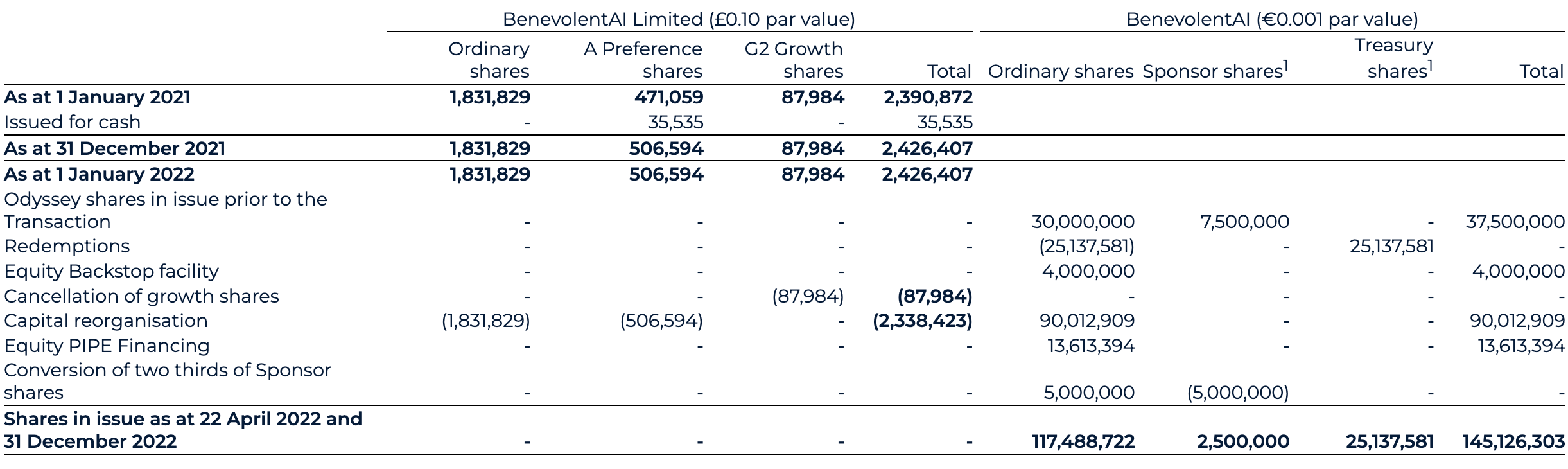

In conjunction with the Transaction, Odyssey entered into subscription agreements with investors (“PIPE Investors”) in a Private Investment in Public Equity transaction (the “PIPE Financing”) in the aggregate amount of €136.1m (£113.0m). In return for their investment, the PIPE Investors received a total of 13,613,394 additional Odyssey Class A shares. An equity back stop facility for €40m (£33.2m) resulted in a further issuance of 4,000,000 ordinary shares were also issued (see note 29). This resulted in a total consideration of £146.2m across the equity PIPE and Backstop, of which £136.7m was received as cash.

Prior to closing, as consistent with the original public share offering by Odyssey, a total of 25.1 million ordinary shares with an agreed redemption price of €9.96 per share were redeemed for cash by eligible ordinary shareholders, following the redemption process. These are currently held as treasury shares. The redemption payable of €250.3m (£207.8m) was paid by Odyssey prior to Transaction close.

As part of the capital reorganisation, BAI Ltd’s share capital was exchanged for shares in Odyssey of £75k, being 90 million shares at a par value of €0.001. This capital reorganisation reflects the transition of the share capital and share premium from BAI Ltd to BenevolentAI. This results in a decrease within share capital of £0.2m from the old share capital (par value of £0.10) with an increase of £584.5m reflecting the share premium as recorded by Odyssey in the share for share exchange. The book value accounted for on consolidation is reflected through a corresponding charge to merger difference of £579.1m, such that the net impact to equity of £5.2m is equal to the net assets acquired of £5.2m.

See note 29 for further details of the share for share exchange.

5 Revenue

We initially recognise income under the AstraZeneca collaborations as deferred revenue, which we become entitled to recognise as revenue in line with the delivery efforts towards the completion of tasks and provision of the deliverables set out in the agreements governing the AZ collaborations. For the year to 31 December 2022, this is represented by a revenue of £10.6m (2021: £4.6m).

Second AZ collaboration

Building on the success of the first collaboration, the relationship with AZ has been expanded into a new 3-year partnership, starting 1 January 2022 and focusing on systemic lupus erythematosus (SLE) and heart failure (HF).

As the result of this collaboration, BenevolentAI received an upfront fee of $15m (£11.8m) in January 2022. As the result of the upfront fee, a total of £2.9m deferred revenue is recognised as of 31 December 2022 (31 December 2021: £nil).

Management have determined that costs directly attributable to the collaboration agreements are immaterial, and consequently cost of sales has not been presented.

There is no related party revenue in the year to 31 December 2022 (year to 31 December 2021: £nil). See note 31 for related party information.

Revenue recognised in relation to contract liabilities since the beginning of each year has been explored further in note 23.

6 Research and development expenditure